Once you have assessed your organization’s market position and developed your organization’s business model, it is time to create your organizational business plan. A business plan is an important tool for identifying and communicating your core capabilities, the value proposition of your products and services, and the customers to whom you will provide products and services. It also explains your financial structure, including costs to run your organization and revenue sources.

A business plan is a living document. Your business plan explains your organization’s strategy and operations: refer to it regularly when you are faced with decisions about priorities or where to invest resources. Update it when your strategies, resources, and underlying assumptions you made in developing the plan change.

What assets and infrastructure do you have available?

What additional assets and infrastructure do you need?

What products and services will you offer? How will you deliver them?

Who are your customers? How will you reach them?

Who are your partners? Who are your competitors?

Who will make which organizational decisions and how?

How will your organization stay financially sound?

Where will your revenue come from, what major costs do you have?

What are your forecasted revenues and costs—when will you break even or become profitable (depending on which is revelant to your business model)?

How Does a Business Model Relate to a Business Plan?

A business model, covered in the Market Position Develop a Business Model handbook, describes the value your organization provides to the market and how you are compensated for your work. It includes information on the following:

The services you provide

The customers you will serve

The assets and infrastructure you will need

Your financial model

Your governance structure.

A business plan, as covered in this handbook, explains how you implement your business model in order to achieve your mission, vision, and goals. It details the organizational and financial structures and processes that you need in place to be able to operate in the capacity you choose.

Your business plan plays an important role in attracting funders, investors, and partners. It is also a key foundation for your organization’s ongoing operational and management functions and plays a large role in informing your program design.

The key aspects of a business plan covered in this handbook are your organization’s:

Assets and infrastructure

Products and services

Market and customers

Partners and competitors

Governance

Financial structure.

The last section of your business plan you should write is the executive summary, which succinctly rolls all of the other sections into an overview focusing on the highlights and strengths of your overall plan.

Related Handbooks

These handbooks provide more detail on designing and implementing a cohesive and balanced residential energy efficiency program.

Develop a plan to implement your financing activities, with defined roles for financial institution partners, contractors, customers, and your program.

Develop contractor engagement, quality assurance, and workforce development plans that include strategies, workflow, timelines, and staff and partner roles and responsibilities.

Step by Step

The steps below describe an approach for organizing your development of a business plan and provide useful resources and examples. Each of the steps corresponds to a section of the plan itself.

You will need to have a clear vision for your business model before you draft your business plan.

Key Resources

For in-depth information about business planning and business models, refer to the following resources:

Download an example of a business plan from DOE’s website to get started, or visit Bplans, a free resource for business planning, to access an online collection of sample business plans.

For business plans specific to delivering building energy efficiency upgrades, you can refer to plans developed by Greater Cincinnati Energy Alliance, a Better Buildings Neighborhood Program partner.

This section of the business plan should describe the assets and infrastructure that allow you to start and run your organization—and the capital and other resources needed to pay for them. It should outline the capabilities required to implement your business model and include:

An overview of your organization—your name, mission, vision, and goals as well as a brief summary of your organization’s services and staff.

Your organization’s legal designation—whether it is for-profit, nonprofit, utility, etc.; its other key characteristics (e.g., tax-exempt status).

Funding requirements for operations—a summary of operational costs, such as leasing office space, staffing, materials, and support services. (These elements will be more fully elaborated in your financial analysis.)

Facility description—the location and quality of facilities, equipment, and other materials needed to operate.

Milestones—a summary of important milestones, expected start and end dates, managers in charge, and budgets for each of the milestones. Experience from many programs suggests that it takes at least one to two years for a new residential energy efficiency program to be fully operational, depending on funding, human resources, availability of qualified contractors, and other factors. That timeframe can be shorter if services are more targeted (e.g., offering insulation installation only, rather than a full suite of energy efficiency upgrades) or are being added to existing efforts.

This section should detail the bundle of services or products your organization will offer, including:

Service/product descriptions—an elaboration of the services described in your business model and the purpose and functions they are intended to address.

Complementary products and providers—based on your market assessment, a description of complementary or alternative products from other organizations, and why yours are unique or meet specific needs of your market.

Sourcing—information about the product and service supply chain, including a description of how your organization intends to obtain its products (i.e., home energy upgrades) and access needed services (e.g., qualified contractors to perform upgrades), as well as whether there are risks to the availability of your inputs (e.g., if only one manufacturer of a particular product is accessible in your market).

Technology—information about what types of technology will be used, such as project tracking software or tools, to support product or service delivery.

Future products—a description of the potential for future product or service development, including expansion into other service areas and market segments.

This section should describe the market for the service or product your organization intends to offer. It will draw upon both your organizational and program market assessments and the description of the customers in your business model. It will provide the foundation for a more detailed analysis of customers as part of your strategy for marketing and outreach. This section should address:

Market identification, size, and trends—a description and analysis of the target market, including sector (e.g., residential, multi-family, commercial), the number of potential customers, trends (e.g., whether home remodels are including home energy upgrades; whether people are converting to different types of heating or cooling sources), and the potential for growth in demand over time, all of which you will have identified during your market assessment.

Market segmentation—the subset of target customers within the market who have common characteristics and needs and for whom you will provide products and services. You should describe how your organization will tailor products and services to meet the specific needs of your market segments.

Marketing, pricing, and promotion strategies—the mix of strategies your organization intends to use to present information, increase demand, and differentiate your service or product. This might include:

A specific market segmentation strategy to target customers in each of the market segments.

A pricing method that best aligns with the needs and behaviors of customers and clients.

Specific promotional tactics, such as advertising and direct marketing. These strategies are outlined in the Marketing and Outreach component.

Value proposition and competitive edge—a description of what makes your product unique and worthwhile investments for consumers and contractors, and why it is better than alternatives, if any, already offered. This section should also describe how your products and services compare with those provided by successful organizations in other places.

This section should identify and describe existing and potential partners and potential competitors. Among other things, this will help you understand how partners can help you establish relationships with your customers and enable effective communications strategies for reaching your target market segments.

Partners—a description of current and future partners, the value they can contribute to your organization, and reasons for engaging them. Highlight any strategic alliances that have been or could be formed and the benefits of doing so.

Competitors—a description of possible competitors and brief descriptions of related products or services, as identified in your market assessment. Highlight the most significant competitors and justifications for competing with them.

This section should introduce the management team responsible for running your organization, define personnel requirements, and describe how your organization will be organized to conduct its activities. It includes:

Organizational structure—a description of how your organization is structured in order to coordinate and conduct its activities and achieve its aims, drawing on your business model.

Management team—names, roles, and responsibilities of leaders. Note any gaps in your organization’s managerial resources and activities, along with the solutions to overcome them.

Personnel plan—personnel requirements, staffing approach, and payroll information. This should include projections of future personnel.

This section of the business plan should comprehensively describe your organization’s current and projected financial structure, including capital and operating costs and revenue forecasts. Defining your financial structure will help you clear a path toward financial sustainability and help you communicate your organization’s financial strength and value to potential funders, investors, and partners.

The descriptions and analysis should include, but not be limited to:

Assumptions—a description of any assumptions in the financial analysis, including assumptions used to project future financial performance. Financial assumptions are critical to business planning because they provide information about your projected revenues and capital and operating costs.

Analysis of alternative assumptions—the financial plan should include a worst case financial scenario, a best case financial scenario, and an expected financial scenario. These scenarios should outline projected surpluses or deficits. The plan should also include a break-even analysis to show the point at which revenues will cover costs. As part of the projection process, you should analyze the impacts of alternative assumptions (e.g., number of upgrades, number of participating contractors) on your organization’s costs and revenues. This will help you understand the sensitivity of results to key assumptions. Any assumptions that cause wide variation may warrant additional analysis and discussion among the organization’s management or other decision-makers. Several methods for analyzing financial scenarios are provided in the presentation Understanding Costs and Revenues, by the Environmental Finance Center at the University of North Carolina at Chapel Hill.

Fundraising strategy and forecast—a forecast of anticipated funding resources over a defined period of time, and a strategy for obtaining these funds.

Financial statements—relevant financial statements presented in a structured and easily understood way. The three basic financial statements that are fundamental to any organization’s business plan are described below along with illustrative examples of each: a balance sheet, income statement, and statement of cash flows. If your organization is not yet operational, use projected financial statements.

Balance Sheet

A balance sheet, also known as a statement of financial position, shows detailed information about your organization’s assets and liabilities. A balance sheet will help your organization ensure that your sources of funds (i.e., your assets) can cover what you owe suppliers, creditors, and others (i.e., your liabilities), which is critical to sustaining your organization over time.

Companies use balance sheets to calculate and report their financial condition at a point in time (e.g., monthly, quarterly, or annually). Balance sheets are essential when closing out a fiscal year. A standard balance sheet usually has three categories: assets, liabilities, and equity (with the organization’s assets balanced by its liabilities and equity). Each category might have many items within it. On the asset side, these may include cash, accounts receivable, and tools and equipment. On the liabilities side, these may include accounts payable, corporate credit card debt, and any bonds the company has issued. The specific items in each category differ by organization and business sector, but every balance sheet must “balance”—that is, the total value of all assets must be equal to all the liabilities and equity.

The following example (for illustration only) is the 2012 annual balance sheet for Coca-Cola Enterprises. All figures are in millions, except share data.

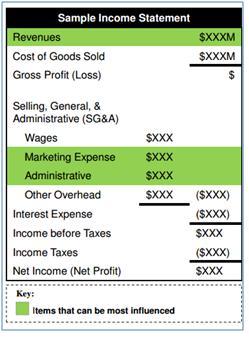

The Income Statement: Revenues, Costs, and Profits

An income statement, also known as a profit and loss statement, is a report of a company’s income, expenses, and profits over a period of time. As part of revenue forecasting, an organization should prepare a projected income statement spanning at least three years. These estimates describe how the organization might perform over time and, when updated and verified, can serve as a tool for future planning and projections.

Income statements allow organizations to track profitability over time. They can also be used as management tools for day-to-day work and as planning tools for the future of your organization. They give funders and partners an understanding of your financial position, needs, and where applicable credit-worthiness.

Income statements detail your organization’s:

Amount and sources of revenue (e.g., grants, foundations, private investors)

Cost of goods and services sold, which are the direct costs attributable to the production of the goods or services sold by your organization (e.g., contractor training, cost of loan buy-down)

Wages based on salary plus benefits packages

Marketing expenses, which might include advertising and direct community outreach campaigns

Administrative expenses

Interest expenses associated with borrowing funds, e.g., interest on loans or lines of credit (note that these are not as applicable for government- or ratepayer-funded organizations)

Net income (or net profit), which is the total amount an organization makes after all expenses have been accounted for; positive net income is critical for an organization to stay viable over time.

Sample Income Statement

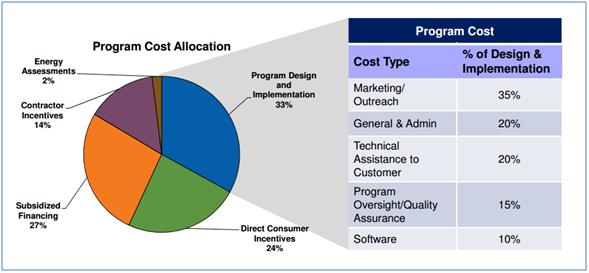

An income statement will help you define all of your costs and revenues. Costs are largely determined by the types of services you will provide.

Certain fixed costs should be expected regardless of size or performance—such as salaries and benefits, office expenses, and marketing. Other costs vary depending on the success of the organization and volume of work. These include financial incentives and subsidies (e.g., rebates, loan buy-downs, contractor training costs) and salaries and benefits for employees who provide demand-sensitive consumer services (e.g., time dedicated to energy concierge services).

The chart below illustrates a residential energy efficiency program cost allocation from the Better Buildings Neighborhood Program Business Model Guide. This is for illustrative purposes only; cost allocations will vary by program.

Residential Energy Efficiency Program Cost Allocation

You can estimate revenues by estimating market demand for your services or products. Every revenue source has a basic set of factors that will determine its amount. The better you understand these, the more accurate the estimates will be.

For example, factors that influence the revenue from charging contractors a fee for participating in a residential energy efficiency program include:

Demand for home energy upgrades

The amount charged by the contractor to provide upgrades

The level of market penetration achieved by the program

The number of participating contractors.

Statement of Cash Flows

A cash flow statement reports on a company's operating, investment, and financing activities. It is reported on a cash basis, which means that it includes only inflows and outflows of cash and cash equivalents. This is in contrast to the balance sheet and income statement, which are reported on an accrual basis that matches revenues to expenses. For example, under a cash-based accounting system, income is counted when cash or a check is received from a customer. Under an accrual-based accounting system, income is counted when a sale is made, even if payment for that sale does not occur until a later date.

The cash flow statement provides information on a firm’s liquidity; an indication of the amount, timing, and probability of future cash flows; and additional information for evaluating changes in assets, liabilities, and equity.

A simple example of an annual projected cash flow, adapted from page 26 of the example business plan from Bplans, is below. It is for illustrative purposes only.

The executive summary encompasses the important points of the entire business plan in no more than two pages. It should highlight the strengths of your business plan and therefore should be the last section of the plan you write. It is usually placed at the beginning of the business plan document.

At a minimum, it should include:

A description of your organization, its mission, objectives, and keys to success

A brief introduction of the management structure

A definition of the industry in which the organization operates

An outlook on the potential future of the organization.

In recent years, hundreds of communities have been working to promote home energy upgrades through programs such as the Better Buildings Neighborhood Program, Home Performance with ENERGY STAR, utility-sponsored programs, and others. The following tips present the top lessons these programs want to share related to this handbook. This list is not exhaustive.

In order to craft a sustainable financial model, organizations need to identify long-term sustainable revenue sources. As with the Better Buildings Neighborhood Program, grant funding can be a great way to get an effort off the ground; however, grant funding does run out, leaving the need to secure alternate revenue sources. Many Better Buildings Neighborhood Program partners overcame this challenge by aligning revenue opportunities with gaps or untapped potential for business in their local market. In some cases, several years were needed to gain trust and demonstrate results before funding was secured, so the sooner you begin considering options, the better the chances are of finding and securing one that is viable. Consider a wide range of options and pursue those opportunities that best match what your organization and local market have to offer. See a detailed list of potential funding sources in the Market Position - Develop a Business Model handbook.

In 2010, St. Lucie County in Florida was awarded an Energy Efficiency and Conservation Block Grant and created the Solar and Energy Loan Fund (SELF), expecting that property assessed clean energy loans (PACE) would be an integral part of the residential loan structure. When Freddie Mac and Fannie Mae challenged the residential PACE system nationwide, SELF shifted direction. They evolved through a multi-year process into a certified community development financial institution (CDFI) focused on energy efficiency and renewable energy upgrades for the residential sector. They targeted low and moderate income populations that had been especially affected in Florida by the economic crisis in 2009.

The change meant that SELF no longer had access to capital from investors seeking highly secured and profitable investments through PACE; however, becoming a CDFI allowed SELF to diversify its products and receive new types of support in the form of grants for technical assistance and loan capital. By becoming a certified CDFI, SELF was able to attract capital from banks as Community Reinvestment Act (CRA) investments and establish legitimacy in the eyes of other socially responsible investors. For example, in the last year of operating under the Better Buildings grant, SELF contacted faith-based foundations that seek to make socially responsible community investments. Over the year and a half after the Better Buildings grant, SELF raised an additional $835,000 from 5 different religious organizations.

Under their business model, SELF faced some challenges limiting their ability to attract capital. For example, even though they implemented new policies to have Uniform Commercial Codes and a more strict collections process, capital providers are still wary of the fact they provide “unsecured” loans. Nevertheless, SELF’s portfolio results of less than 1% default and less than 3% delinquency helped prove that they had a good evaluation method and their risk management procedures were effective. The new CDFI business model allowed SELF to become self-sufficient by providing a platform to offer financial and non-financial services that could generate diversified revenue streams. These revenue sources include interest and fees earned on their investments; fees from off balance sheet portfolios such as commercial PACE; and fees from partnering with other financial institutions to sell their financial product and other activities such as contractor training.

Resources

The following resources provide topical information related to this handbook. The resources include a variety of information ranging from case studies and examples to presentations and webcasts. The U.S. Department of Energy does not endorse these materials.

This strategic plan describes the goals, objectives, market, and business model for the Greater Cincinnati Energy Alliance's energy efficiency program and service offerings.

This business plan introduces Southern California Gas Company (SoCal Gas) and the company's vision and goals. It provides detailed strategies and approaches for achieving goals, as well as budgets for activities.

This business plan is organized into nine chapters. Chapter I provides background on the business plan concept and describes the organization of Southern California Edison Company's (SCE's) plan. Chapter II presents SCE's vision of EE in California, including discussion of important policy issues. Chapter III provides a summary of SCE's proposed EE portfolio including: SCE's vision and goals; drivers of EE; high-level strategies to achieve its vision; how SCE will comply with the requirements for statewide administration and third-party solicitations; key portfolio data such as budget, forecast energy and demand savings, cost-effectiveness; and proposed metrics.

This business plan outlines Pacific Gas and Electric Company's (PG&E's) high-level approach to achieving state energy efficiency policy goals through 2025.

This business plan outlines California Central Coast Regional Energy Network's (3C-REN) core design elements - the crucial component of a phased implementation approach to overcome potential barriers, forecasted budget requirements - and shows how measuring success with a comprehensive set of metrics and tools will lead to the anticipated program improvement outcomes and market transformation goals.

This business plan outlines the Bay Area Regional Energy Network's (BayREN) ten-year vision, with goals, strategies, and tactics to increase the access and availability of energy efficiency services to a broad range of ratepayers and sectors, including moderate income residents, multifamily property owners, small and medium commercial businesses, and local government municipalities.

Glenn Barnes, Environmental Finance Center at The University of North Carolina at Chapel Hill

Publication Date

Presentation aimed at program administrators that highlights the elements of an income statement, methods for forecasting costs and revenues, the importance of performance measurement, and potential revenue streams.

The Market Position & Business Model Implementation Plan Template will help you develop a strategy for planning, operating, and evaluating your business planning activities.

This report serves as a resource for program administrators and building contractors who are or may be interested in starting or expanding their services into the residential energy efficiency market.