Once you and your lending partners have made design decisions, it is time to develop an implementation plan for financing in conjunction with your program’s energy upgrade services to create an overall positive customer experience.

Assuming your financing activities are part of a larger effort by your program to promote the uptake of home energy upgrades, you will be developing one overall implementation plan that addresses all aspects of your program (e.g., Financing, Marketing & Outreach, Contractor Engagement & Workforce Development).

The financing activities that will be addressed in your program’s implementation plan will depend on the financing design decisions you have made. When accounting for your financing activities in your implementation plan, consider the following steps:

Identify the actions required to implement your financing activities

Document the flow of funds

Establish staffing requirements and roles/responsibilities

Develop a timeline for key milestones and a budget for implementing your financing activities

Share your implementation plan with your lending partners.

This handbook provides you with step-by-step information on what to consider when incorporating your financing activities into your program’s implementation plan, tips for success from past energy efficiency programs that achieved success in the marketplace, and resources that can assist with the development of your financing implementation plan.

As you begin to implement your financing activities, you will learn what strategies are working well and those that may require refinement. Remaining flexible and accounting for a continuous improvement process in your program implementation will help to ensure sustained program success.

Related Handbooks

These handbooks provide more detail on designing and implementing a cohesive and balanced residential energy efficiency program.

Develop contractor engagement, quality assurance, and workforce development plans that include strategies, workflow, timelines, and staff and partner roles and responsibilities.

Elements of financing activities for which you (or your participating lending partners) may need to develop a plan for include:

Sources of capital and options for recapitalizing loan funds

Loan activity roles, responsibilities, and timelines (e.g., pre-approvals, origination, servicing and collection, underwriting, application processing, and funding of loans)

Management of credit enhancement funds (if applicable)

Coordination of contractor payments

Marketing and outreach to identify and reach new customers

Post-upgrade review prior to disbursement of loan proceeds

Coordinating loan origination and disbursement with rebate processing

Integration with existing utility rebate programs.

You may need to plan for additional activities as well, depending on your program design.

To accomplish these and other financing activities, your implementation plan could include resources related to administration and decision making such as:

A flow chart describing tasks, assignments, and due dates

An organizational chart and staffing plan describing roles and responsibilities of your program and your lending partners

Specific work rules and procedures (policies and procedures) related to applications, disbursements, and other steps

Map of capital flows between the program, lender, and (if applicable) secondary markets or investors

Project timelines with key milestones, including dependencies (i.e., X must be completed before Y can begin)

Your plan may also include infrastructure planning related to IT systems and software for managing loans and integration with project data (i.e., tracking upgrade projects and status of loans).

Many program managers choose to start with goals and objectives when designing implementation plans—i.e., identifying a key objective (e.g., accept loan applications on April 1) and outlining all of the materials, resources, and process flows needed to accomplish that objective.

For more information on financing activity resource requirements, see Chapter 10 of DOE's Clean Energy Finance Guide for Residential and Commercial Building, “Resource Requirements.”

Implementation Plans From Better Buildings Neighborhood Program Partners

Boulder, Colorado’s EnergySmart program produced a detailed action plan with activities, deliverables, and timelines by phase and task.

Community Power Works of Seattle, Washington, has created a planning document with flowcharts and tables designed to help guide both the initial launch of the program and its ongoing development.

Michigan Saves has an extensive program overview that features a detailed program design schematic (including capital flows) and outlines roles for all partners during each step of the program process.

Developed by the U.S. Department of Energy, the Financing Implementation Plan Template will help you develop a strategy for planning, implementing, and evaluating your financing activities.

A critical component of the implementation plan related to your financing activities is to determine and document the specific flow of capital between the capital provider, program administrators, lenders, secondary markets (if applicable), and borrowers. Capital flows include funds for loans, interest-rate buy-downs, credit enhancements, and other funding purposes.

Documentation of your capital flows typically will include the following components:

A description of your program’s capital sources and subsidies or enhancements, if any (e.g., interest rate buy-down, loan loss reserve, senior or subordinate capital, debt service reserve)

The accounts that will be required to deliver the program (e.g., accounts to fund loan loss reserves, subordinate capital investments, individual loans)

The process for funding these accounts

The policies and procedures for managing these accounts

The criteria for releasing funds.

Your lending partner(s) can help you document the capital flows for your program.

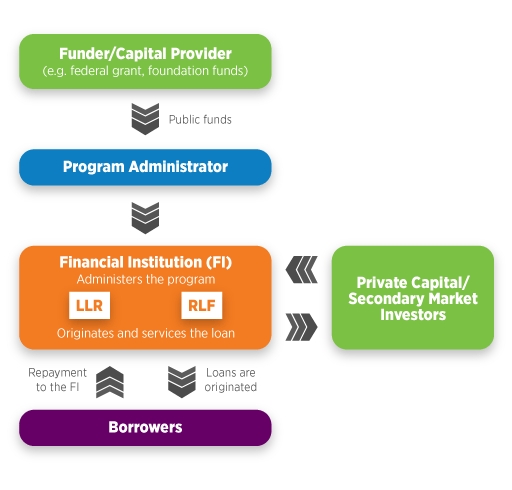

Below is an example of a capital flows schematic used by many Better Buildings Neighborhood Program partners. Generally, these programs used public money for credit enhancements or revolving loan funds. This example schematic illustrates the flow of funds between a capital provider, the program administrator, lenders, secondary market investors, and borrowers where a loan loss reserve (LLR) or revolving loan fund (RLF) is used.

Example Capital Flow Schematic

Source: U.S. Department of Energy, 2014.

One potential stakeholder involved in the flow of capital not shown in the above schematic is contractors. Working with contractors and lenders, your program can provide what is often called a “dealer loan,” under which a contractor offers financing on behalf of the lender, eliminating the need for the borrower to engage with an additional party (the lender). Because most programs involve several partner organizations, a customized flowchart will help you track, monitor, and move funds. Your program’s capital flow schematic should illustrate the flow of funds between all relevant stakeholders (e.g., the public sector, private capital providers, your lending partners, contractors, secondary market investors, borrowers).

Another key step of implementing your financing activities is ensuring that you have the correct internal staff to help manage your activities, and that they have clearly defined roles and responsibilities. The lending agreements you make with lenders will outline the activities and responsibilities expected of these institutions, but internal staff (which might include a hired consultant) that understand and can manage your program’s financing activities will greatly contribute to your program’s success.

The key determinant in deciding the level of staff financing expertise required to implement your program is whether you will simply sponsor the financing activities of others, manage capital to fund loans and/or credit enhancements, or directly perform the origination and servicing functions. Better Buildings Neighborhood Program partners relied on a mix of staff and consultants to provide financial expertise.

Examples of programs that relied on program staff for financing expertise:

NeighborWorks of Western Vermont performs origination and servicing activities, and trained existing staff with financing experience to originate energy efficiency loans.

Examples of programs that rely primarily on consultants for financing expertise:

Michigan Saves oversees a network of lenders and manages a credit enhancement fund. They have operated the program with assistance from staff that serve as consultants to the State of Michigan during the design process and by training employees in the management of the credit enhancements during operations.

EnergySmart in Boulder County, Colorado, utilized a consultant to design its financing program, including identifying a lending partner (Elevations Credit Union) and structuring a credit enhancement. EnergySmart also trains its mostly non-financial employees and energy advisors on its financing offerings.

Enhabit, formerly Clean Energy Works Oregon, oversees a network of lenders and manages a credit enhancement. The program initially used a consultant to help design the program and financial process, and provide assistance with training of their non-financial staff. Enhabit later hired a financial expert to provide these services in-house.

The financial expertise you need and your staff’s specific roles will be dependent on the design decisions you make. The following table summarizes the level of staff financial expertise recommended based on the role of your program.

Source: U.S. Department of Energy, 2014.

An organizational chart and staffing plan describing roles and responsibilities of your program as well as your lending partners is an effective way to capture the decisions you’ve made into your overall implementation plan.

For more information on financing activity resource requirements, see Chapter 10 of DOE's Clean Energy Finance Guide for Residential and Commercial Building, “Resource Requirements.”

After you have identified all of the actions needed to implement your financing activities, you will want to organize them into a timeline and develop a budget to identify what financial resources are required. Project timelines can include dependencies (i.e., X must be completed before Y can begin), and identify who will be responsible for each task or action. Your overall program budget will dictate the resources available to implement your financing activities. Once you develop a budget for your financing activities you may find that you need to revisit your design decisions and make refinements to your financing activities.

Your lending partners can provide important feedback on your implementation plan, enabling you to maximize their contributions in your program, appropriately allocate resources, and bolster program awareness. Soliciting and incorporating comments and feedback from your lending partners about your implementation plan can also foster cooperation and facilitate the smooth development of your loan products and delivery of your financing services.

The level of information required by various stakeholders will vary depending on their role. For instance, you can communicate your implementation plan with a local contractor association by providing a slide deck that describes the loan product and the various participants and diagrams the process flow. A lending partner or provider of a credit enhancement will likely want a detailed description of all elements of the program, which could be provided with a policies and procedures manual.

Tips for Success

In recent years, hundreds of communities have been working to promote home energy upgrades through programs such as the Better Buildings Neighborhood Program, Home Performance with ENERGY STAR, utility-sponsored programs, and others. The following tips present the top lessons these programs want to share related to this handbook. This list is not exhaustive.

Financing can be a complicated topic for programs, and having staff with financing knowledge and expertise can be very valuable. Financing program administration involves working with lenders and understanding how they operate as well as understanding financial regulatory issues and loan product features. Several Better Buildings Neighborhood Program partners hired staff or consultants with financing skills and knowledge, which helped to launch programs more quickly and efficiently, and administer them effectively over time.

Enhabit, formerly Clean Energy Works Oregon, initially used a consultant to help design their financing products, which began with the pilot program through the City of Portland in 2009. Enhabit later hired a financing expert to serve as a lender relations manager to attract additional lenders and to create strategic partnerships that leverage private capital. Leveraging in-house expertise, the program created five lending partnerships with a CDFI, a regional bank, and three credit unions, which enabled more than $50 million in capital for home upgrades. Enhabit staff understanding of bank and credit union financing, in addition to efforts to ensure compliance with required regulations, have been key factors in successfully attracting and retaining lenders. Through its network of pre-qualified contractors, the program is able to offer financing options that are convenient with competitive rates and flexible terms.

Michigan Saves works to create a one-stop shop for energy efficiency financing through their Home Energy Loan Program. To facilitate a smooth process for both homeowners and participating lenders, Michigan Saves hired staff with financing expertise. Financing staff helped to attract and provide ongoing coordination with the nine credit unions currently participating in the program (as of early 2014). Staff work with participating credit unions to make adjustments to loan design and process (when needed), ensure that non-financial staff at Michigan Saves understand the program’s loan offerings, and coordinate lending activities with participating contractors. Through June 2014, the Michigan Saves Home Energy Loan Program made more than 3,600 loans representing an investment of nearly $30 million.

New Hampshire’s Beacon Communities Project relied heavily on staff financing expertise to create its successful program. New Hampshire’s program was awarded to, and administered by, the New Hampshire Office of Energy and Planning (OEP). OEP contracted with the Community Development Finance Authority (CDFA) to assist with implementation of the project. CDFA staff managed homeowner outreach, and served as direct liaisons to local municipalities, utilities, property owners, lenders, auditors, and building contractors. New Hampshire’s program included the use of loan loss reserves (LLR), interest rate buy-downs, and co-lending with local banks. Establishing the bank partnerships and agreements needed to implement these financing mechanisms was spearheaded and managed by a CDFA staff person with prior financial program experience. As the program moved beyond the Better Buildings grant period, OEP continues to rely on financing experts to provide guidance related to the LLR needed, the percentage of bad debt which the bank should write-off prior to charging the program, and current market interest rates. In total, ten local banks and credit unions made over 150 loans through their partnership with NH Better Buildings during the grant period of 2010-2013.

Homeowners do not benefit from access to financing if they don’t know about or understand options available to them. Contractors are often the primary transaction point for selling upgrades, and many programs have found that ongoing collaboration with contractors through sales training, regular meetings, and requests for feedback can foster greater understanding and sales of program loan products. Some successful programs have staff in a contractor manager role to organize trainings, address questions and concerns, and overall coordinate relationships with participating contractors. Along with simplifying the financing application process, working with contractors to integrate financing into the home performance sales process avoids making financing another complicated decision point for customers.

EnergyWorks of Philadelphia recognized that contractors can have a tremendous influence on homeowner decisions about how to pay for an energy upgrade. The program therefore trained contractors on how to effectively make affordability of energy efficiency a key part of every sales proposal and assessment. Contractors were also trained on how to better utilize special financing and monthly payment plans to increase both their closing rates and market penetration for more energy efficient home improvements. In addition, EnergyWorks provided contractors with program-sponsored technical training for BPI and RESNET certification, if needed, streamlined the energy assessment process and developed a consistent customer report template, and used an integrated software platform to provide maximum efficiency and customer service to contractors during loan/incentive origination, administration, payment, and reporting. Between 2010 and 2013, EnergyWorks helped finance over 1,900 residential upgrade projects, totaling more than $17 million.

Enhabit, formerly Clean Energy Works Oregon, works with its contractors to provide business coaching, peer mentoring, business development classes, business accounting, and sales training. Supporting the development of these skills is a key factor in Enhabit’s success. Trainings include discussion of Enhabit’s loan offerings and eligible lenders, and how financing is a valuable tool to help drive sales. These trainings were well-received by contractors and helped them improve their business processes, making them more profitable. Between program launch in March 2011 and December 2013, Enhabit’s close relationship with its contractor partners resulted in the completion of more than 3,000 upgrades. For more information on how Enhabit partners with their contractors, see the case study Making the Program Work for Contractors.

The Greater Cincinnati Energy Alliance (GCEA) recognized that the best way to drive demand for home energy upgrades was to involve local contractors that worked in homes on a daily basis. To that end, GCEA identified, trained, and mentored contractors who were interested in promoting the benefits of energy efficiency and saw it as a means to expand their business. Through a network of participating contractors, homeowners throughout Greater Cincinnati ultimately purchased energy efficiency upgrades and services totaling almost $19 million. Between program launch in 2011 and November 2013, GCEA issued 127 residential loans, totaling more than $1 million with no losses.

In October 2010, Austin Energy rolled out its single-family residential energy "Best Offer Ever" promotion, a three-month special that combined rebates and no-interest loans for energy upgrades. Austin Energy offered extra contractor training on the financing to drive sales during the promotion. Once draft promotional plans were in place, Austin Energy hosted a breakfast meeting—getting on their Home Performance with ENERGY STAR contractors’ schedules before they were out in the field for the day—to discuss the plans and collect feedback from the contactors. Contractors provided feedback on the launch plans, received sample forms, and were trained on how to use them. The contractors were also candid about their involvement in implementing the offer. Most contractors had not actively marketed financing options before, so Austin Energy walked the group through each party’s role and responsibility in the loan process. Austin Energy also scheduled the promotion during the fall and winter, which is typically a slow season for building contractors in otherwise sunny and hot Texas—increasing the likelihood that projects would be completed in a timely manner while also helping contractors avoid seasonal layoffs. As a result of the promotion, a total of 568 participants received Home Performance with ENERGY STAR upgrades through 47 contractors in six months—more than 10 times Austin Energy's typical participation rate.

As part of the ShopSmart with JEA program, Jax Metro Credit Union (JMCU) worked closely with contractors by holding regular meetings (monthly or quarterly) as well as lunch and learn opportunities to educate contractors on the loan options available. The credit union also did outreach to contractors or contractor associations in the community recognizing that the contractors would play an important role in selling benefits of the loan product. It was a long process, nearly 14 months, before the relationship between the credit union and the contractors was fully developed. From 2010-2012, ShopSmart with JEA completed 206 residential upgrades. JMCU members completed more than $1.2 million worth of energy upgrades on 183 homes in the community, and JEA and JMCU financed nearly 90 percent of completed upgrades.

Lenders can be a valuable partner for programs in marketing loan products and driving demand for home energy upgrades. They are often a trusted source of information in a community, and they have access to potential customers and partners such as existing customers, loan aggregators, and large property investors and managers. Many Better Buildings Neighborhood Program partners found success by co-marketing their programs with lenders to expand loan uptake and, ultimately, the number of home energy upgrades completed. Programs often accompanied co-marketing with training about the program, so that lending partners and their staff could respond to homeowner questions about program services, in addition to the loan products.

Boulder County, Colorado’s EnergySmart program partnered with Elevations Credit Union to develop and deliver low-interest financing for eligible energy efficiency improvements for homes. Residential loans start at $500 at interest rates of 2.75% with the option of 36-, 60-, 84- and 120-month terms. The financing launch occurred in August 2012, and EnergySmart leveraged Elevations Credit Union’s marketing channels and co-branded itself with the lender to promote the low-interest loans. Tactics included creating a webpage dedicated to energy loans on Elevations Credit Union’s website; social marketing, including Facebook, Twitter, and blog promotion; and events/promotions at Elevations Credit Union branches. EnergySmart complemented these joint efforts with direct mailers, bus ads, bike-sharing ads, print ads, and a large radio campaign. Over $1.7 million in energy loans were issued by EnergySmart between August 2012 and September 2013, helping 150 homes and businesses overcome cost barriers to energy efficiency investment.

The Local Energy Alliance Program (LEAP) of Charlottesville, Virginia, partnered with the University of Virginia Community Credit Union (UVA CCU) to offer residential energy loans. After discussions with LEAP early on, UVA CCU moved forward on its own to establish the Green $ense loan option for participants in the LEAP program. Later, the credit union became a sponsor of the FHA PowerSaver loan with assistance from LEAP. While no formal relationship between LEAP and the credit union was established, the UVA CCU PowerSaver program encourages customers to participate in the LEAP Home Performance with ENERGY STAR program by posting links to the program on its website, conducting joint marketing with LEAP, and verbally referring customers to the LEAP program. To obtain a PowerSaver loan, UVA CCU simply requires that a homeowner meet FHA’s eligibility requirements. As partners, LEAP and UVA CCU maintain open lines of communication; however, because they have not entered into a formal agreement relative to funding the program, LEAP does not receive data on loan activity from UVA CCU. Nevertheless, both parties have been satisfied with their partnership to date.

RePower Kitsap partnered with two local credit unions, first Kitsap Credit Union (KCU) and then later Puget Sound Cooperative Credit Union (PSCCU), to offer low-cost home energy loans to its community in Washington. RePower found that it was crucial to educate the lenders’ internal staffs about the program’s requirements, goals, and priorities. RePower held in-house trainings for appropriate lending staff at KCU branches. They also walked KCU staff through a diagnostic energy assessment at one of the credit union staff member’s homes. In the early days, several RePower customers contacted the credit union to inquire about the loan and were told “We don’t offer this type of loan.” RePower found that this internal training greatly increased KCU staff’s awareness about the energy efficiency and the available loan product. In addition to training lending partner staff, RePower encouraged KCU and PSCCU to assign specific staff to manage the energy efficiency loan process, connect with RePower staff, review applications and eligible measures, and evaluate various work scopes that might be included in a loan—all with the goal of improving the customer experience and driving uptake of home energy loans. By ensuring that lending staff are properly trained and by encouraging KCU and PSCCU to have a financing point person, RePower is able to leverage its program outreach efforts with those of its lending partners. A total of 71 loans totaling nearly $700,000 were issued by KCU and PSCCU during the Better Buildings Neighborhood Program grant period. PSCCU is continuing to offer and market loans throughout the region despite the grant period end.

Resources

The following resources provide topical information related to this handbook. The resources include a variety of information ranging from case studies and examples to presentations and webcasts. The U.S. Department of Energy does not endorse these materials.

New York State Energy Research and Development Authority (NYSERDA)

Because of its potential to reduce customers’ first costs and leverage private funds, financing has been increasing in importance as a strategy for facilitating energy upgrades as program administrators seek to meet ambitious goals in a shifting energy efficiency landscape. This paper evaluates the experience of BBNP grantees to identify how programs can most effectively integrate loan offerings into their broader efforts to promote energy efficiency upgrades. The paper also identifies best practices from grantees’ experience related to integrating financing into program outreach and trade ally interactions.

This planning document from Community Power Works of Seattle, Washington, includes flow charts and tables designed to help guide both the initial launch of the program, which includes setting goals, and its ongoing development.

This summary from a Better Buildings Residential Network peer exchange call focused on how loan performance data is tracked and analyzed, and what the data shows.

Presentation providing an overview of financing programs, a strategy for continuous improvement, tools for program management, a risk management strategy, and common risks associated with financing programs.

This website provides an overview of financing as it pertains to state, local, and tribal governments who are designing and implementing clean energy financing programs. Residential financing tools include residential PACE (R-PACE), on-bill financing and repayment, loan loss reserves and other credit enhancements, revolving loan funds, and energy efficient mortgages.

Montana Alternative Energy Revolving Loan Program,

Palm Desert Energy Independence Program,

Sonoma County Energy Independence Program,

Sustainable Connections: Energy Challenge,

Texas LoanSTAR

This U.S. Environmental Protection Agency resource is intended to help state and local governments design finance programs for their jurisdiction. It describes financing program options, key components of these programs, and factors to consider as they make decisions about getting started or updating their programs.

New York State Energy Research and Development Authority (NYSERDA)

This report provides an overview of considerations for designing and implementing successful energy efficiency financing programs for existing buildings in the residential and commercial sectors. Information on key issues related to energy efficiency financing programs, guidance to existing resources that provide more in-depth financing program design and implementation information, and strategies for delivering broad customer access to attractive financing products that enhance customer capacity and willingness to invest in energy efficiency to address "first cost" barriers are included.

This report provides an overview of the fundamentals of energy efficiency financing program planning and design and provides tools for deciding the objectives and mechanics of EE financing initiatives. The report walks policymakers and program administrators through key questions that must be resolved to better understand what efficiency financing can be reasonably expected to achieve, and for whom.