Everything you have prepared so far has put you in a position to implement your financing activities. To prepare yourself for program delivery, you should have completed the following steps:

Designed your financing activities, which are likely focused on sponsoring an existing loan product or program or providing capital to lenders, either to lend directly or as a credit enhancement.

Developed an implementation plan that identifies workflows and defines the roles for your program, lenders, and contractors, as well as an evaluation plan and metrics to help you track and measure program progress.

Developed financing resources internally and externally that will enable you to perform the core financing functions of your program.

To successfully deliver financing as part of your program, take the following steps:

Prepare to implement your financing activities.

Consider a soft launch or pilot to test systems, workflows, and processes.

Launch your financing activities and manage them over time, including adjustments to program design based on feedback from stakeholders (e.g., contractors, homeowners, lending partners), and from analysis of metrics and data in your financing evaluation plan.

Related Handbooks

These handbooks provide more detail on designing and implementing a cohesive and balanced residential energy efficiency program.

Implement marketing and outreach activities in coordination with other program components to generate demand for your program's services.

Step by Step

Delivery of your financing activities should occur in coordination with the launch of your residential energy efficiency program. Specific steps for financing are described below:

Before launching your financing activities, you will want to strive to have the key mechanisms in place, while remaining flexible to allow for the continuous improvement of your program as you gain experience. If you have followed the stages described in the Financing handbooks, you have:

Offer financing solutions that work best for your community

Partner with lenders and contractors who can help drive the uptake of home energy improvements, and encourage higher-cost upgrades than customers might otherwise find possible, which can result in deeper energy savings

Define roles and responsibilities for you and your partners, and put in place the right work, capital, and process flows to guide your actions

Hire and train staff knowledgeable about your financing activities, and ensure your lender and contractor partners are supportive of your program’s mission and ready for program implementation

Develop the policies, procedures, and documents needed to execute your financing activities

To ensure a more seamless delivery of your financing activities that enhance the uptake of home energy loans, you may want to consider a soft launch or pilot to test the financing systems, workflows, and processes you have put in place.

A soft launch is the quiet startup of a program, making it available to a limited number of participants or working with a limited number of lenders or contractors.

A pilot program is designed to test a concept or approach to determine if a more significant investment in the approach is justified.

Once you confirm that you have everything in place to implement your financing activities, and have tested your systems, workflows, and processes through a soft launch or other mechanism, you are ready to launch your financing program in coordination with your program’s other activities.

As you launch your financing activities, be sure you are prepared to manage them over time based on feedback from homeowners, contractors, and lending partners to allow for the continuous improvement of your financing strategy.

Consider the following areas for optimizing delivery of your financing activities:

Manage key tasks. You can choose to do this internally or in collaboration with one or more of your partners (e.g., lenders, contractors, marketing firms). Key tasks include performing marketing and outreach, certifying contractors to participate in your program, processing loan applications, underwriting (approving/rejecting applications) and originating loans, servicing loans, processing collections activities, charging-off defaulted loans, and managing credit enhancements.

Maintain quality assurance (QA) and quality control (QC) activities. QA and QC programs ensure the continual success and integrity of your program. You will want to make sure that the processes you have put in place with your lending and contractor partners to deliver home energy loans are working and creating a positive customer experience.

Manage funds and cash flow. This activity ensures that the flow of cash between your program, capital providers, lenders, contractors, secondary market investors, and borrowers (identified in your implementation plan) is working efficiently with appropriate management and oversight of funds.

Provide performance management for financing staff. Just as QA or QC is important for your program processes, it is also important to evaluate the performance of your financing staff. Routine evaluations for staff create individual accountability and an opportunity to improve staff interactions.

Generate and distribute regular reports. Through routine reports (monthly, quarterly, semi-annually, or annually) on the progress of your financing activities, you can identify gaps or ways to improve your program implementation. These reports can also serve as helpful literature for other communities looking for “lessons learned” to help develop their own energy upgrade programs.

Manage relationships with partners. Your partnerships with lenders, contractors, and other stakeholders are critical to increasing loan uptake. Be sure to maintain constant communication with your partners to resolve issues that arise and ensure a seamless program delivery.

In October 2010, Austin Energy rolled out its single-family residential energy "Best Offer Ever" promotion, a three-month special that combined rebates and no-interest loans for energy upgrades.

The Best Offer Ever promotion offered customers who signed up for an energy upgrade between October 1 and December 31, 2010, the opportunity to receive both a rebate and low-interest financing (0–8% interest rate for 3- to 10-year loans based on loan length, measures installed, and customer credit history) that had a combined value of approximately $2,300 per household.

During the three-month period the program received more than 600 applications. As a result of the promotion, a total of 568 participants received Home Performance with ENERGY STAR upgrades through 47 contractors in six months—more than 10 times Austin Energy's typical participation rate.

Detailed Planning Process to Avert Bottlenecks

A detailed planning process was critical to the successful launch of the program. Austin Energy thought through each step of the various work streams that would be needed to deliver the Best Offer Ever promotion and developed a comprehensive series of flowcharts to document the associated needs. The planning process and tools were instrumental in identifying program weaknesses and averting potential bottlenecks. Visit Examples for other flowcharts developed by programs.

Designing the Program to Benefit Both Homeowners and Contractors

In keeping with Austin Energy’s desire to streamline the customer experience and mitigate up-front costs for both homeowners and contractors, Best Offer Ever was designed to allow customers to assign their rebates directly to contractors, who in turn reduced homeowners’ invoices by the rebate amount. In parallel, Austin Energy developed an expedient contractor payment system that delivered electronic rebate reimbursement directly to contractors within two weeks. Additionally, Austin Energy offered extra contractor training on the financing to enable sales, and scheduled the “Best Offer Ever” promotion during the fall and winter, which is typically a slow season for building contractors in otherwise sunny and hot Texas—increasing the likelihood of projects being completed in a timely manner and helping contractors avoid seasonal layoffs.

Plan, Adjust, and Learn

Even with extensive pre-launch planning, the Best Offer Ever promotion was a learning experience. Karl Rábago, Vice President at Austin Energy, noted, “Planning for success is harder than planning for failure…Take notes and learn, as this is a long run opportunity. Capturing and honoring your errors will help you identify what you need for next time and build incrementally as your program develops.”

One unanticipated challenge that Austin Energy faced—and overcame—during the promotion was the expiration of loan preapprovals. Contractors were so overwhelmed with work that loan preapprovals were expiring before the energy upgrades were completed. Austin Energy responded by working with the lender to send out weekly notices to contractors to keep them informed of when their customers’ loan pre-qualifications were due to expire so that they could prioritize those jobs in their work scheduling.

Following the brief but high-volume Best Offer Ever promotion, program staff paused to incorporate process improvements, hire additional support, and carefully design and test several pilot programs.

Program Results to Date

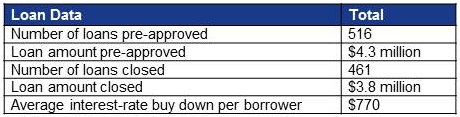

Since October 2010, Austin Energy has rolled out a variety of program offerings, including a multifamily program (launched in April 2012) and a single-family program (launched in October 2012). Austin Energy’s single-family and multifamily programs have resulted in the completion of more than 3,800 energy upgrades with an expected annual energy savings of over 20%, or about $2 million per year in savings for program participants.

The following table summarizes the key loan data for the single-family program between October 2012 and January 2014:

In recent years, hundreds of communities have been working to promote home energy upgrades through programs such as the Better Buildings Neighborhood Program, Home Performance with ENERGY STAR, utility-sponsored programs, and others. The following tips present the top lessons these programs want to share related to this handbook. This list is not exhaustive.

Complicated loan and program application processes have deterred many potential customers from following through with an upgrade. Delays and overly burdensome requirements raise barriers to participation. Many programs have successfully employed strategies to reduce the number of requirements that homeowners must meet in order to receive a loan, and to speed the processing of loan applications so projects can proceed quickly once a homeowner decides to move forward.

Enhabit, formerly Clean Energy Works Oregon, worked with Craft3, a non-profit community development financing institution (CDFI), to help more homeowners qualify for loans and streamline the loan application process. Their approach was to use utility repayment history as a proxy for credit. Craft3’s underwriting process includes a credit score check and review of other debt obligations (e.g., bankruptcies, liens, judgments); however, Craft3 examines utility bill repayment history in lieu of analyzing an applicant’s debt to income ratio (DTI). This approach significantly reduces loan underwriting expenses for Craft3, helps to simplify the loan application process for homeowners, and allows for quicker approvals. Between March 2011 and December 2013, Craft3 completed more than 2,600 loans valued at $33.4 million, with an average loan amount of $12,500. While the loans have been made for only a few years, loan default rates have been below industry averages.

Pennsylvania's Keystone Home Energy Loan Program, administered by AFC First Financial Corporation in partnership with EnergyWorks Philadelphia and the Pennsylvania Treasury Department, worked with multiple lenders to provide quick-approval unsecured energy efficiency loans up to $15,000, often within two hours of receiving the application. This was accomplished by underwriting based on a minimum credit score (640 or higher), 50% debt ratio requirement, and income and employment information (as stated by the borrower, rather than verified via the employer). Approximately 70% of applicants are approved for loans. The combination of minimum credit score, debt ratio and other factors used in underwriting allows AFC First to streamline the application process while minimizing risk of borrowers defaulting on their loans. Between 2010 and 2013, EnergyWorks was able to help finance over 1,900 upgrades, totaling more than $17 million.

Homeowners do not benefit from access to financing if they don’t know about or understand options available to them. Contractors are often the primary transaction point for selling upgrades, and many programs have found that ongoing collaboration with contractors through sales training, regular meetings, and requests for feedback can foster greater understanding and sales of program loan products. Some successful programs have staff in a contractor manager role to organize trainings, address questions and concerns, and overall coordinate relationships with participating contractors. Along with simplifying the financing application process, working with contractors to integrate financing into the home performance sales process avoids making financing another complicated decision point for customers.

EnergyWorks of Philadelphia recognized that contractors can have a tremendous influence on homeowner decisions about how to pay for an energy upgrade. The program therefore trained contractors on how to effectively make affordability of energy efficiency a key part of every sales proposal and assessment. Contractors were also trained on how to better utilize special financing and monthly payment plans to increase both their closing rates and market penetration for more energy efficient home improvements. In addition, EnergyWorks provided contractors with program-sponsored technical training for BPI and RESNET certification, if needed, streamlined the energy assessment process and developed a consistent customer report template, and used an integrated software platform to provide maximum efficiency and customer service to contractors during loan/incentive origination, administration, payment, and reporting. Between 2010 and 2013, EnergyWorks helped finance over 1,900 residential upgrade projects, totaling more than $17 million.

Enhabit, formerly Clean Energy Works Oregon, works with its contractors to provide business coaching, peer mentoring, business development classes, business accounting, and sales training. Supporting the development of these skills is a key factor in Enhabit’s success. Trainings include discussion of Enhabit’s loan offerings and eligible lenders, and how financing is a valuable tool to help drive sales. These trainings were well-received by contractors and helped them improve their business processes, making them more profitable. Between program launch in March 2011 and December 2013, Enhabit’s close relationship with its contractor partners resulted in the completion of more than 3,000 upgrades. For more information on how Enhabit partners with their contractors, see the case study Making the Program Work for Contractors.

The Greater Cincinnati Energy Alliance (GCEA) recognized that the best way to drive demand for home energy upgrades was to involve local contractors that worked in homes on a daily basis. To that end, GCEA identified, trained, and mentored contractors who were interested in promoting the benefits of energy efficiency and saw it as a means to expand their business. Through a network of participating contractors, homeowners throughout Greater Cincinnati ultimately purchased energy efficiency upgrades and services totaling almost $19 million. Between program launch in 2011 and November 2013, GCEA issued 127 residential loans, totaling more than $1 million with no losses.

In October 2010, Austin Energy rolled out its single-family residential energy "Best Offer Ever" promotion, a three-month special that combined rebates and no-interest loans for energy upgrades. Austin Energy offered extra contractor training on the financing to drive sales during the promotion. Once draft promotional plans were in place, Austin Energy hosted a breakfast meeting—getting on their Home Performance with ENERGY STAR contractors’ schedules before they were out in the field for the day—to discuss the plans and collect feedback from the contactors. Contractors provided feedback on the launch plans, received sample forms, and were trained on how to use them. The contractors were also candid about their involvement in implementing the offer. Most contractors had not actively marketed financing options before, so Austin Energy walked the group through each party’s role and responsibility in the loan process. Austin Energy also scheduled the promotion during the fall and winter, which is typically a slow season for building contractors in otherwise sunny and hot Texas—increasing the likelihood that projects would be completed in a timely manner while also helping contractors avoid seasonal layoffs. As a result of the promotion, a total of 568 participants received Home Performance with ENERGY STAR upgrades through 47 contractors in six months—more than 10 times Austin Energy's typical participation rate.

As part of the ShopSmart with JEA program, Jax Metro Credit Union (JMCU) worked closely with contractors by holding regular meetings (monthly or quarterly) as well as lunch and learn opportunities to educate contractors on the loan options available. The credit union also did outreach to contractors or contractor associations in the community recognizing that the contractors would play an important role in selling benefits of the loan product. It was a long process, nearly 14 months, before the relationship between the credit union and the contractors was fully developed. From 2010-2012, ShopSmart with JEA completed 206 residential upgrades. JMCU members completed more than $1.2 million worth of energy upgrades on 183 homes in the community, and JEA and JMCU financed nearly 90 percent of completed upgrades.

Lenders can be a valuable partner for programs in marketing loan products and driving demand for home energy upgrades. They are often a trusted source of information in a community, and they have access to potential customers and partners such as existing customers, loan aggregators, and large property investors and managers. Many Better Buildings Neighborhood Program partners found success by co-marketing their programs with lenders to expand loan uptake and, ultimately, the number of home energy upgrades completed. Programs often accompanied co-marketing with training about the program, so that lending partners and their staff could respond to homeowner questions about program services, in addition to the loan products.

Boulder County, Colorado’s EnergySmart program partnered with Elevations Credit Union to develop and deliver low-interest financing for eligible energy efficiency improvements for homes. Residential loans start at $500 at interest rates of 2.75% with the option of 36-, 60-, 84- and 120-month terms. The financing launch occurred in August 2012, and EnergySmart leveraged Elevations Credit Union’s marketing channels and co-branded itself with the lender to promote the low-interest loans. Tactics included creating a webpage dedicated to energy loans on Elevations Credit Union’s website; social marketing, including Facebook, Twitter, and blog promotion; and events/promotions at Elevations Credit Union branches. EnergySmart complemented these joint efforts with direct mailers, bus ads, bike-sharing ads, print ads, and a large radio campaign. Over $1.7 million in energy loans were issued by EnergySmart between August 2012 and September 2013, helping 150 homes and businesses overcome cost barriers to energy efficiency investment.

The Local Energy Alliance Program (LEAP) of Charlottesville, Virginia, partnered with the University of Virginia Community Credit Union (UVA CCU) to offer residential energy loans. After discussions with LEAP early on, UVA CCU moved forward on its own to establish the Green $ense loan option for participants in the LEAP program. Later, the credit union became a sponsor of the FHA PowerSaver loan with assistance from LEAP. While no formal relationship between LEAP and the credit union was established, the UVA CCU PowerSaver program encourages customers to participate in the LEAP Home Performance with ENERGY STAR program by posting links to the program on its website, conducting joint marketing with LEAP, and verbally referring customers to the LEAP program. To obtain a PowerSaver loan, UVA CCU simply requires that a homeowner meet FHA’s eligibility requirements. As partners, LEAP and UVA CCU maintain open lines of communication; however, because they have not entered into a formal agreement relative to funding the program, LEAP does not receive data on loan activity from UVA CCU. Nevertheless, both parties have been satisfied with their partnership to date.

RePower Kitsap partnered with two local credit unions, first Kitsap Credit Union (KCU) and then later Puget Sound Cooperative Credit Union (PSCCU), to offer low-cost home energy loans to its community in Washington. RePower found that it was crucial to educate the lenders’ internal staffs about the program’s requirements, goals, and priorities. RePower held in-house trainings for appropriate lending staff at KCU branches. They also walked KCU staff through a diagnostic energy assessment at one of the credit union staff member’s homes. In the early days, several RePower customers contacted the credit union to inquire about the loan and were told “We don’t offer this type of loan.” RePower found that this internal training greatly increased KCU staff’s awareness about the energy efficiency and the available loan product. In addition to training lending partner staff, RePower encouraged KCU and PSCCU to assign specific staff to manage the energy efficiency loan process, connect with RePower staff, review applications and eligible measures, and evaluate various work scopes that might be included in a loan—all with the goal of improving the customer experience and driving uptake of home energy loans. By ensuring that lending staff are properly trained and by encouraging KCU and PSCCU to have a financing point person, RePower is able to leverage its program outreach efforts with those of its lending partners. A total of 71 loans totaling nearly $700,000 were issued by KCU and PSCCU during the Better Buildings Neighborhood Program grant period. PSCCU is continuing to offer and market loans throughout the region despite the grant period end.

Many programs struggle with communicating the value of financing to homeowners. Financing can be a complicated topic, and ensuring that homeowners understand how their loans work and the benefits they will realize is important for converting interest into action. Many Better Buildings Neighborhood Program partners achieved success by simplifying messages, focusing on those that convey long-term value, low monthly payments, low interest rates, enhanced home comfort, and energy savings.

The Keystone Home Energy Loan Program (Keystone HELP) found that “Low Monthly Payments” and “No Money Down” were effective messages to help drive loan uptake. They also advertise that homeowners will not encounter any surprises down the road. For example, the program website states, “Keystone HELP offers True Fixed Rate Financing, which means the rate of your loan will never change, and your low monthly payment will stay the same for the life of your loan.” This gave homeowners confidence that their monthly payments would be stable, and encouraged homeowners to make a larger investment in energy efficiency improvements to their home. As of October 2013, the program has provided more than $100 million in financing to over 11,000 Pennsylvania homeowners for energy efficiency home improvements.

Enhabit's, formerly Clean Energy Works Oregon, messaging around financing focuses on affordability, home transformation, home comfort, home health, and proven results. For example, their website includes statements such as:

“It has never been more affordable to transform your home from vintage looker to cutting edge performer.”

“Hundreds of other homeowners have already financed a CEWO Home Energy Remodel, with costs ranging from $2,000 and $30,000 and an average just over $10,000. In most cases the money they save helps offset a nice chunk of the monthly loan payment.”

“We think that’s a pretty good deal for a more comfortable, healthier, and energy efficient home.”

Enhabit couples its messaging with a simplified loan process and provides sample estimates of monthly loan costs and expected energy savings so homeowners can readily make informed decisions about the costs of their upgrade and expected savings in terms of monthly cash flow.” Between March 2011 and December 2013, Enhabit, through lending partner Craft3, completed more than 2,600 loans valued at $33.4 million, with an average loan amount of $12,500.

When speaking with homeowners considering upgrades, Boulder County, Colorado’s EnergySmart program focuses on the messages that upgrades are a path to homeowner benefits, such as comfort, health and safety, and reduced energy bills. They also focus on how financing can be combined with available rebates to make upgrades financially attractive to homeowners. For example, their website states, “Energy Loans can help you achieve a more efficient, comfortable and affordable home. Interest rates start as low as 2.75%. Loans can be paid in part or in full with zero prepayment penalties. Energy Loans can be combined with rebates to fully fund your home upgrades.” By simplifying messages and the loan process, in conjunction with energy advisor support, Boulder County was able to achieve conversion rates of greater than 70%. Between October 2010 and September 2013, EnergySmart was designed, launched, and supported the completion of upgrades in more than 4,100 homes. Over $1.7 million in energy loans were issued by EnergySmart between August 2012 when the loan product became available and September 2013, helping 150 homes and businesses overcome cost barriers to energy efficiency investment.

Resources

The following resources provide topical information related to this handbook. The resources include a variety of information ranging from case studies and examples to presentations and webcasts. The U.S. Department of Energy does not endorse these materials.

This case study features New York City Energy Efficiency Corporation (NYCEEC), a member that focuses on financing energy efficiency and clean energy upgrades for multifamily buildings in the city and surrounding communities.

Ivy Knoll Senior Retirement Community used PACE financing to make significant building improvements of systems that were outdated or energy inefficient. Through PACE financing, Ivy Knoll management was able to select improvements that had the highest energy savings but also came with higher upfront costs for the 7-story, all-electric building.

New York State Energy Research and Development Authority (NYSERDA)

With project funding from Energize NY PACE and incentives from NYSERDA's Multifamily program, Natlew Corporation was able to make energy efficiency upgrades to their multifamily affordable housing complex in Mount Vernon, NY.

PACE Equity worked closely with CRE Investment Financing to develop and fund a new construction, micro-apartment project in the Sloans Lake area of Denver. This project is the first new construction PACE project in Colorado, as well as the first PACE project completed in Denver.

This policy brief provides insight into the transaction of an on-bill energy efficiency loan portfolio between two mission-oriented lenders, Craft3 in Oregon and Self Help in North Carolina.

California Statewide Communities Development Authority

Publication Date

This document defines consumer protection policies for California's statewide Open PACE program, which is implemented at the local level for residential and commercial property owners. Property assessed clean energy (PACE) programs enable homeowners to finance energy efficiency, renewable energy, and water efficiency improvements. These recommended consumer protection policies can help guide PACE Program implementation to ensure homeowners realize maximum benefit.

New York State Energy Research and Development Authority (NYSERDA)

Publication Date

Organizations or Programs

New York State Energy Research and Development Authority (NYSERDA)

Two visual flow charts, one that illustrates the process starting with customer interest to final incentive payment, and another that illustrates the program's quality assurance process.

This summary from a Better Buildings Residential Network peer exchange call focused on how organizations can diversify and grow new revenue streams and types of financing approaches used to make resources stretch further and help homeowners finance upgrades. Speakers include Connecticut Green Bank, Sealed, and Craft3.

This summary from a Better Buildings Residential Network peer exchange call focused on how loan performance data is tracked and analyzed, and what the data shows.

This presentation covers lesson learned for PACE from the Toledo Port Authority, innovative real estate finance solutions from the Ygrene Energy Fund, and financing energy improvements on utility bills.

This presentation provides an overview of energy efficiency financing for low- and moderate-income households, including a sector overview, consumer protections, financing products, and lessons learned.

This presentation describes how PG&E is using advanced metering infrastructure (AMI) to enhance their advanced home upgrade whole-house retrofit program, on-bill financing, and residential pay for performance (P4P) program.

Presentation providing an overview of financing programs, a strategy for continuous improvement, tools for program management, a risk management strategy, and common risks associated with financing programs.

Financial Program Management for Continuous Improvement

This website provides an overview of financing as it pertains to state, local, and tribal governments who are designing and implementing clean energy financing programs. Residential financing tools include residential PACE (R-PACE), on-bill financing and repayment, loan loss reserves and other credit enhancements, revolving loan funds, and energy efficient mortgages.

This report provides an overview of the current state of on-bill programs and provides actionable insights on key program design considerations for on-bill lending programs.

This SEE Action report offers state and local policymakers, state utility regulators, program administrators, financial institutions, consumer advocates and other low- and moderate-income (LMI) household stakeholders an understanding of the relationship between LMI communities and energy efficiency; lessons learned from existing energy efficiency financing programs serving LMI households; and the financing products these programs use and their relative advantages and disadvantages.

This report examines participation of low and moderate income borrowers (LMI) in the first WHEEL portfolio. This is the first report in a multiyear project by EPC on Residential Energy Finance and the LMI Market that will take a close look at the market for residential energy efficiency and renewable energy loans to in order to increase the number and rate of the retrofits they facilitate.

This report on clean energy finance programs provides state and local government officials with a comprehensive resource on residential PACE history, legal and financing structures, terms and administrators. The report described how the program works, how local governments can set up their own programs and how they are financed. The report further describes PACE's growth, the legal challenges it has faced thus far, and consumer protection concerns that have been raised by consumer advocates.

These policies provide protections for homeowners using PACE to invest in clean energy, energy efficiency, and water efficiency home upgrades. The standards address eligibility, repayment, disclosures, privacy concerns, contractor conduct, and operational requirements for PACE Programs.

Montana Alternative Energy Revolving Loan Program,

Palm Desert Energy Independence Program,

Sonoma County Energy Independence Program,

Sustainable Connections: Energy Challenge,

Texas LoanSTAR

This U.S. Environmental Protection Agency resource is intended to help state and local governments design finance programs for their jurisdiction. It describes financing program options, key components of these programs, and factors to consider as they make decisions about getting started or updating their programs.

New York State Energy Research and Development Authority (NYSERDA)

This report provides an overview of considerations for designing and implementing successful energy efficiency financing programs for existing buildings in the residential and commercial sectors. Information on key issues related to energy efficiency financing programs, guidance to existing resources that provide more in-depth financing program design and implementation information, and strategies for delivering broad customer access to attractive financing products that enhance customer capacity and willingness to invest in energy efficiency to address "first cost" barriers are included.